After a challenging period for fixed-income markets, conditions look to be right for a better year in bonds according to Aviva Investors.

• The reasons behind the optimistic outlook for government bonds and credit

• Why EM asset prices should remain resilient

• The risks to look out for in 2024

After years of low interest rates, we saw a sudden regime change in 2022 following the waning of the COVID-19 pandemic and Russia’s invasion of Ukraine. As inflation spiked, central banks embarked on rapid and aggressive interest-rate hikes to arrest it, leading to steep losses across most asset classes, including fixed income.

At the start of 2023, lower energy prices and the reopening of the Chinese economy brought a glimmer of hope: that tighter monetary policy would tame inflation while avoiding a recession. While major economies did manage to avoid slipping into recession last year, there was still plenty of uncertainty about, with bank failures creating market jitters in the US and Europe in early spring and continued geopolitical concerns.

For the bulk of the year, broad corporate bond indices remained flat and sovereign bonds nursed more losses (albeit much smaller than those in 2022). Then, in November, came a late plot twist: the best month for bonds in 40 years, with market sentiment aided by a change in tone from the US Federal Reserve (Fed), which suggested it was more amenable to rate cuts than markets had previously thought, given the resilience of the US economy. A consensus formed that inflation was becoming less of a threat and the peak in interest rates had already been reached – or at least was in sight – across the US, UK and euro zone.

Also read: A History of Price Collection and How the CPI Has Been Measured

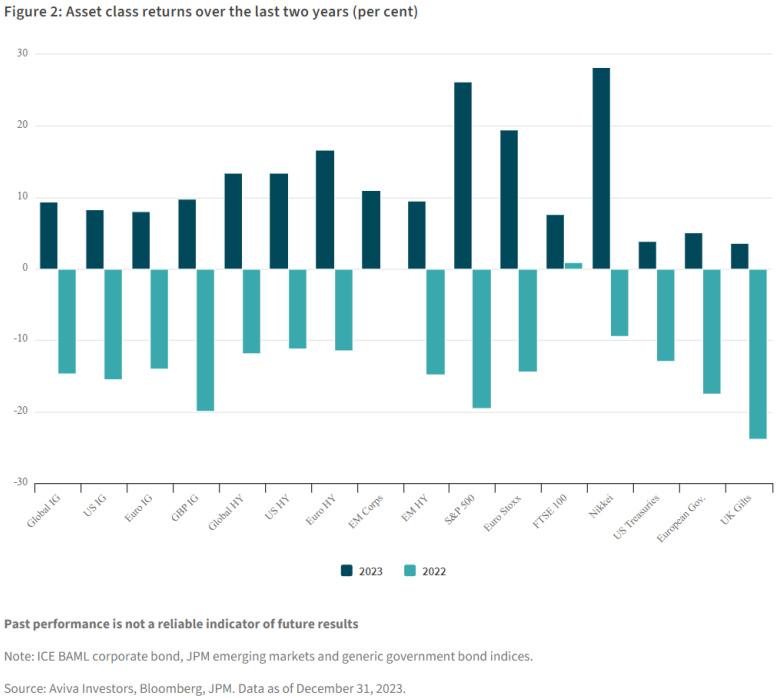

The market rally helped most asset classes deliver a strong performance for the year and the possibility of an easier ride in 2024 (see Figure 1). But given lingering concerns over recession risks, inverted yield curves, sticky core inflation, large fiscal deficits and continuing geopolitical tensions, what does the risk/reward picture look like for bonds over the next 12 months?

The income is back in fixed income

It should be remembered that bonds do not require economic growth to deliver returns. Low or falling growth, and a stable or falling outlook on inflation, are enough to generate reasonable all-in yields (see 2023 returns, as shown in Figure 2). Following the rate moves seen over the last two years, risk-free rates remain close to their highest levels in a long time. Hence, while the pace of rate cuts will dictate the magnitude of returns for all asset classes, bonds are back on the menu for return-seeking investors.

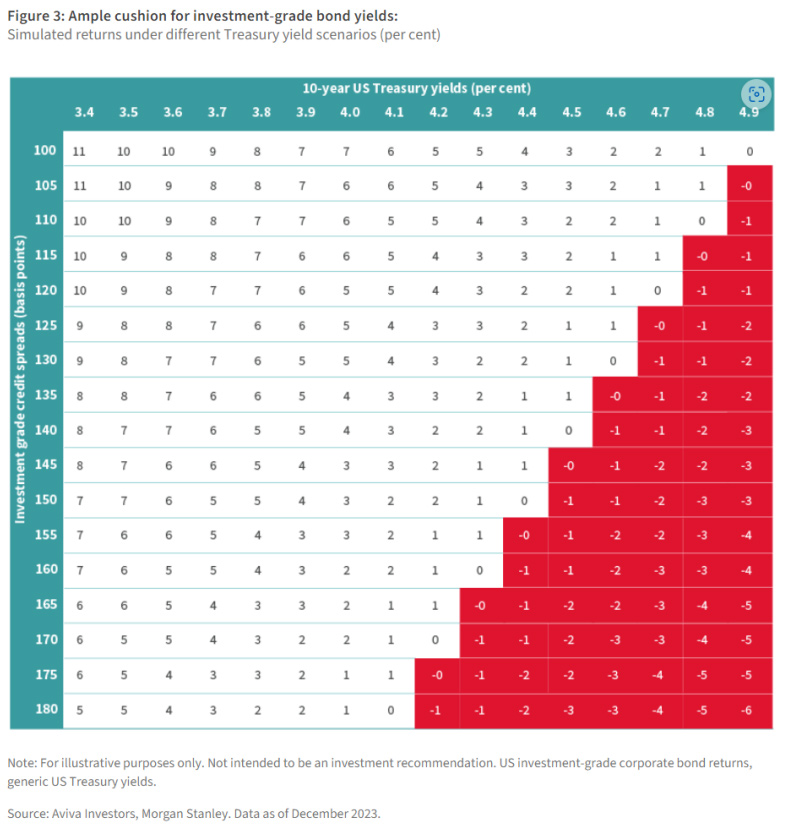

Even if rate cuts don’t materialise at the pace the market is currently expecting, higher starting yields should offer investors more protection if global growth slows faster than expected or inflation remains stubbornly high. To illustrate, Figure 3 is a simple simulation of possible returns for investment-grade corporate bonds under different US Treasury yield scenarios.

Further, the current global macro backdrop looks supportive for total returns across all fixed-income asset classes in the coming year. As detailed in our latest House View, both growth and inflation projections lend support to the view we are heading for a soft landing, particularly in the US.

Of course, there are risks to this outlook, notably a harder landing than expected and, consequently, higher rates persisting for longer than is currently priced in by the markets. A series of elections in major developed and emerging economies in 2024 could also complicate matters. In the following, our fixed income teams offer their thoughts on what the year ahead holds for bonds.

1. The outlook for government bonds

2024 is expected to be a much better year for government bond returns, as the end of the monetary tightening cycle in most major markets leads to a renewed focus on the timing of policy easing and rate cuts. Market optimism on these factors was the fuel for the impressive rally that occurred in the last two months of 2023.

Our expectation is that income will be the main driver of returns for government bonds and we believe there is limited potential for capital losses, given central banks appear to have reached the end of their hiking cycles. As policy eases, the extent of any price uplifts or capital appreciation will depend on whether monetary policymakers deliver more than is already priced in.

We expect to see a moderate slowdown in economic growth in 2024, and therefore policy easing is likely to happen at a measured pace. This would mean any capital appreciation would be moderate, but when combined with the prevailing attractive income on offer, total returns on government bonds could be strong and make them relatively attractive compared with other asset classes on a risk-adjusted basis. Inflation is expected to continue to fall over the course of 2024, which would further increase the attractiveness of government bonds as a diversifier in a portfolio that also contains equities (because high inflation hurts both bonds and equities, it tends to increase the correlation in performance between the two asset classes).

On the other hand, there is likely to be a significant amount of sovereign bond issuance for the markets to digest in 2024, which could prove a concern. Whether there is sufficient demand to meet this new supply will likely be dependent on the strength or otherwise of the economic backdrop.

We believe investors should be more comfortable owning developed market sovereign bonds, given we are likely at the peak of interest rates, with inflation (though still sticky) continuing to fall and unemployment rates coming off their lows in advanced economies. The potential for some central banks’ quantitative tightening (QT) programmes to end, pause or change in their make-up (in terms of speed, maturity or type of bonds being targeted), may allow markets room to breathe, in which case, the level of developed market sovereign bond issuance will likely become less of a concern – particularly so if rate cuts begin to come through. Furthermore, with elections looming in both the US and the UK, the likelihood of increased fiscal pledges from candidates has the potential to keep term premia elevated.

The only exception to the easier policy picture in 2024 within developed markets is Japan, where the Bank of Japan (the central bank) is expected to tighten policy this year and likely bring an end to negative interest rates. Japanese bond yields should remain elevated for some time, but when and if they move lower, the change is expected to be far less significant than that of their developed world counterparts.

2. The outlook for credit

Last year proved to be a good year for corporate bond (credit) markets. The rise in bond yields and credit spreads in 2022 gave investors an attractive entry point into 2023. Higher key interest rates provided comfort there would be a cushion against any spread widening in the event of an economic contraction. And the wide dispersion in investment-grade and high-yield bonds alike provided plenty of relative value opportunities for investment. For those who took advantage, total returns were compelling, with most of the returns derived from the coupon income.

Moving into 2024, the picture looks bright. Dispersion is still wide, presenting active managers with more opportunities for bottom-up stock selection, while 2023’s higher interest rates should provide an even larger cushion against any spread widening.

Investment grade: Yields remain attractive

After the aggressive rate hikes of the last two years, investment-grade corporate bonds offer appealing risk-adjusted returns via a combination of attractive all-in yields and the potential for capital gains as yield curves normalise. There is a reasonable cushion in the yields on offer, which would have to move at least 80 basis points (bp) higher in order to deliver a negative total return over the next 12 months.

The income element is an important factor in the attraction of corporate bonds. Cash might have been king in 2023, but we believe income will dethrone it in 2024. While there may still be question marks as to whether developed economies are heading towards a soft landing or a recession, it is worth noting again that bonds do not need economic growth to continue to deliver income.

Nevertheless, cash instruments will likely continue to present a challenge to credit through the first half of 2024, as investors justifiably question the wisdom of investing in a corporate bond offering the same yield as a “risk-free” cash instrument. However, while interest rates may remain higher for longer, given that major central banks look to be at, or near, the peak in their interest rate cycles, cash rates look destined to fall. This means it might well be a good time to consider locking in the elevated income on offer from investment-grade bonds.

While we remain optimistic about all-in yields and the potential for a positive total return for global investment-grade bonds in 2024, we are also proceeding with caution. Credit market technicals are sound and fundamentals for the asset class remain in reasonable shape. Although companies will face higher financing costs going forward, many issued long-dated bonds when yields were close to their alltime lows in 2020, making the maturity wall for refinancing in the sector less of a concern compared to issuers further down the credit spectrum.

As for valuations, credit spreads are looking rich and remain at very tight levels. The broad US investment-grade market had an option-adjusted spread of 104 bp at January 11, 2024, a level not seen since February 2022, just before Russia’s invasion of Ukraine. This makes us cautious on valuations and wary of extending our credit exposure too far down the credit curve.

Our investment process lends itself to markets without a direction as we choose companies and sectors based on their correlation to each other. Currently we believe there is enough dispersion in investment grade for bottom-up stock pickers to harness alpha (or excess returns).

High yield: Watch the looming maturity wall and idiosyncratic risk

Global high yield, along with other risk assets, breathed a sigh of relief during 2023, having finished the year without the much-anticipated recession. Consequently, investors were able to earn a high total return well above the already high starting yield of the asset class.

In 2024, the technical backdrop remains supportive. The deluge of fallen angels in 2020 (formerly investment-grade bonds that suffered ratings cuts to junk status) helped improve the average rating of the market, though most of this debt has since rebounded back into investment grade. Taken together with the dearth of issuance in the past two years, the size of the high-yield market has shrunk significantly, which can be a supportive technical tailwind to credit spreads and prices.

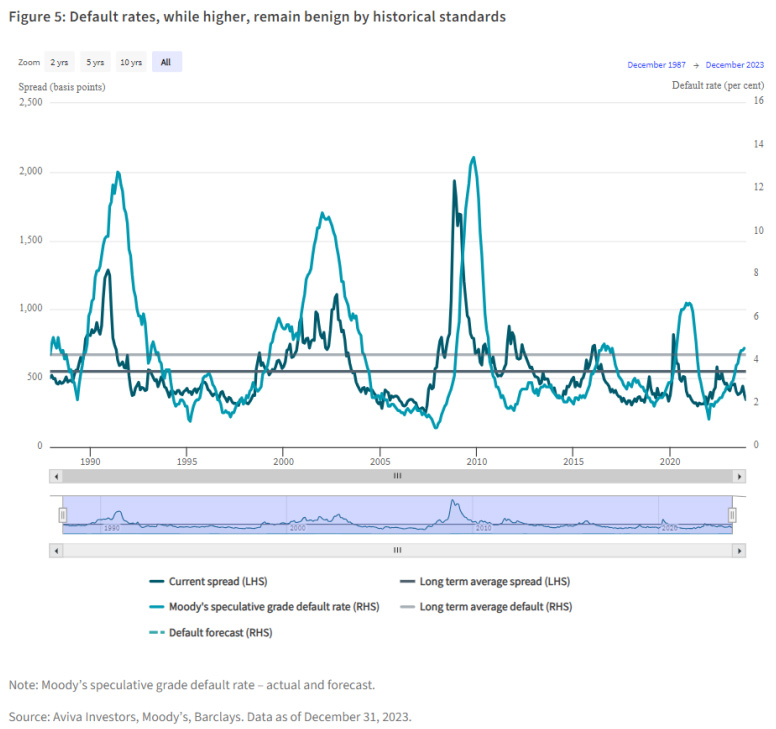

Though increased in 2023, defaults have been the bright spot in the asset class in the past couple of years (Figure 5). Despite higher interest rates, most high-yield issuers continue to benefit from the ultra-low coupons of bonds issued during 2020-2021. However, that benefit will soon come to an end as maturing bonds are refinanced. The impact will be most dramatic among lower-quality issuers. We expect to see an uptick in liability management exercises, such as debt buybacks or exchange offers to reduce overall debt levels. But these options will not be available to all issuers, and we anticipate an increase in the default rate for lower-quality corporates. We expect overall defaults to be between four per cent and 4.5 per cent in 2024, in line with the long-term average.

Finally, yields above eight per cent, as seen in 2022-23, are historically rare. Historically, when they have breached this level, the subsequent 12-month total return projection has been positive, averaging double-digit growth. While there has been a slight compression in yields since the start of the year, all-in yields still remain attractive. Corporate credit spreads, however, are below historical averages and on fundamental reasons alone, we believe are likely to remain rangebound and unlikely to compress from here.

We expect to see low economic growth and further falls in inflation this year – with inflation remaining above central bank targets. In the past, economic scenarios such as this have been commensurate with “credit repair” when companies focus on repaying liabilities.

However, the extended period of central bank hiking is likely to increasingly feel “recessionary” for some sectors, for example consumer discretionary, where higher borrowing costs, tighter lending standards and lower wage inflation are cumulatively taking effect. Therefore, while the overall macro backdrop is likely to be resilient and supportive for global high yield, an increase in idiosyncratic risk is expected from This document is for professional clients/qualified investors only. It is not to be distributed to, or relied on by retail clients. Page 10 Aviva Investors: Internal levered sectors and issuers that need to adjust to lower growth and roll refinancings into higher yields. This makes careful credit selection even more critical in 2024.

An advantage of a global strategy is the ability to seek and deliver returns through diversification. In recent months, sterling and euro high yield bonds have outperformed their US counterparts. We prefer European high yield as wider spreads in this market make it attractive relative to the US. Multi-currency issuers also present opportunities, where we have the advantage of allocating to the most attractive bond regardless of its currency.

3. The outlook for emerging-market debt

Given the multiple crises, big and small, that have rocked economies and markets over recent years it is astonishing how resilient emerging market (EM) asset prices have remained. If this year sees a continuation of the resilience theme, it could bring enticing total returns across both hard- and localcurrency EM debt during 2024.

Interest-rate cutting cycles in EM, supported by developed-market monetary easing, are likely to help local-currency returns, and the disinflationary trend across most markets should continue this year. Limited energy inflation and cooling food prices should contribute to this dynamic. While most of the easing in inflation so far has been a result of improvements in supply, slowing demand could start to play a more prominent role.

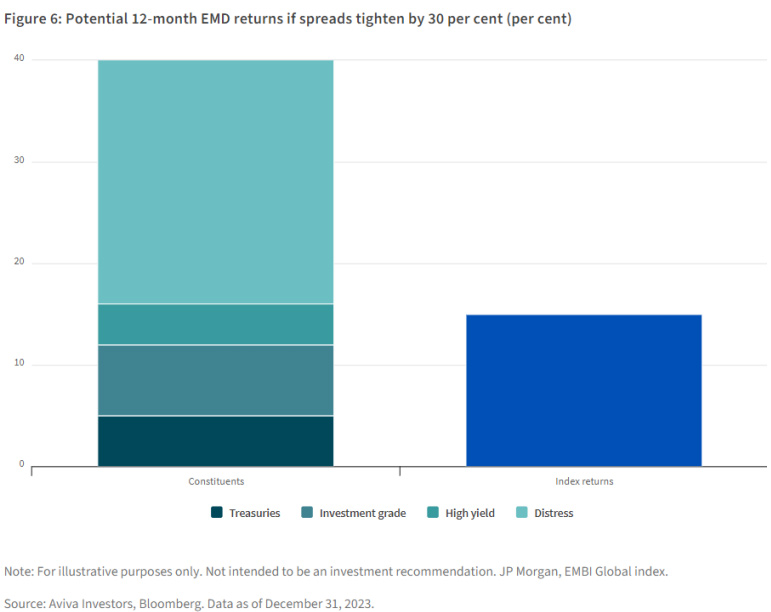

We are optimistic on the prospects for EM hard-currency returns in 2024. With US bond yields now likely past their peak, we anticipate high-single-digit return potential for EM debt, assuming a hard landing for the global economy is avoided. Being selective remains key, however.

Looking at the three main groups of issuers, within the higher-rated issuer category, spreads do not look especially compelling and nominal yields are attractive relative to history. Among middle-rated issuers, high-yield names with strong fundamentals still offer decent spread pick-up over US Treasuries and scope for further spread compression. At the lower end of the ratings spectrum, distressed and defaulted debt also looks to offer value on a selective basis.

While investors may need a resumption of inflows and more stability in core rates to see significant upside potential, bonds from countries like Egypt, which we expect to muddle through, and Ecuador, which has been overly penalised by markets for perceived political risk in the wake of a surge in gang violence, could provide interesting opportunities over the medium term.

If 2023 turned out to be the year of distressed hard-currency debt, then this year we think will be the turn of local frontier debt. Egypt, Nigeria and Turkey could start to look interesting very shortly, if not already. For that we need capital flows to return to the asset class, a broadly stable macro backdrop and continued sensible domestic policies, which should combine to reduce the fear of further currency weakness.

So, what are the hazards to look out for in 2024? Supply-chain pressures could bring challenges, given the recent droughts affecting the Panama Canal, the impact of El Niño weather patterns and attacks on shipping lanes in the Red Sea. And, while the disinflation narrative remains intact, the bar for another sharp move lower in inflation is very high at this stage.

EM debt investors must also monitor the election cycle. Around three quarters of all people living in democracies will be voting in 2024, with the vote for the US presidency likely the most hotly contested. While the number of EM countries holding elections is among the largest ever, not many of these votes are expected to be materially market moving. After all the action of 2023 in Argentina, Turkey and This document is for professional clients/qualified investors only. It is not to be distributed to, or relied on by retail clients. Page 12 Aviva Investors: Internal Poland, among others, 2024 should feel less eventful – although one always needs to be alert to potential surprises.

4. The bottom line

Writing any outlook is fraught with risks and this year is no exception. However, we believe that bond investors can look forward to the rest of 2024 with confidence, thanks to the following three broad developments:

• The move from rate hikes to rate cuts, which should provide a positive tailwind to fixed-income returns;

• Strong technicals and benign default rates, alongside relatively high starting yields, providing a cushion in periods of volatility;

• Attractive idiosyncratic opportunities for active managers to exploit, given the elevated level of dispersion between issuers.

")

Bets and Embrace EM Debt")

Platform To Digitally Trade Corporate Bonds")