With Indian debt set to be included in major international benchmarks this year, emerging-market sovereign debt analyst Nafez Zouk from Aviva Investors travelled to the country to assess its prospects.

Read this article to understand:

• Why the entry of Indian debt into international benchmarks will be welcomed by emerging market investors

• Why the rapid pace of economic growth should help keep the country’s fiscal deficit in check

• Why the quality of India’s institutions helps offset political risk as elections get underway.

Few countries leave such a lasting impression on the visitor as India, steeped in a rich history, and captivating in the intensity of its sights, sounds and smells.

From the moment my plane came in to land in Mumbai, I had a sense of what to expect. Down below, the hustle and bustle of one of Asia’s largest and most vibrant cities was plain to see.

On the way to my hotel, as the taxi driver navigated snarled traffic criss-crossing construction sites for new metro lines, I caught sight of coastal highway expansions and new bridges, indicating the vast scale of the infrastructure projects being undertaken.

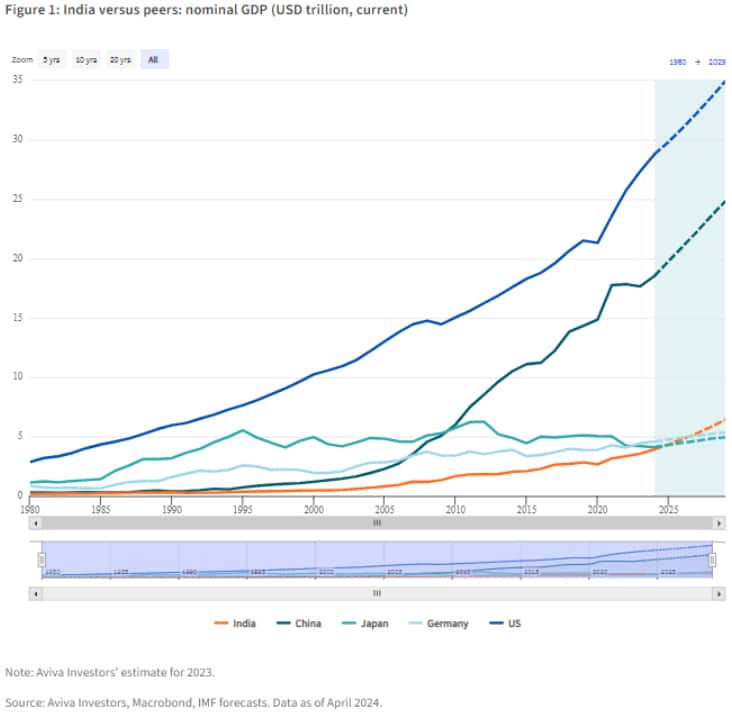

Here was visible evidence of the pace of India’s economic growth. According to our estimates, real GDP expanded seven per cent in 2023 and nine per cent the prior year. The International Monetary Fund predicts India will become the world’s third-biggest economy by the end of the decade, perhaps sooner, overtaking Germany and Japan (see Figure 1).

India’s economic trajectory, coupled with the fact its bonds will soon be listed on the widely tracked JP Morgan Government Bond Index-Emerging Markets (BGI-EM) indices for the first time, have prompted a great deal of excitement among international investors. Ahead of the country’s general election, which started this month and will run until June, I visited to investigate India’s outlook, the prospects for its bond market and the direction of policy.

Positive trends

India remains an extremely poor country – about 60 per cent of its nearly 1.3 billion people live on less than US$3.10 a day, the World Bank’s median poverty line – but the situation is changing rapidly.1 A 2023 report by the United Nations Development Programme said the proportion of the population living in multidimensional poverty – a measure of deprivation across monetary poverty, education, and basic infrastructure services – had fallen to 16.4 per cent by 2021, down from 55 per cent in 2005.

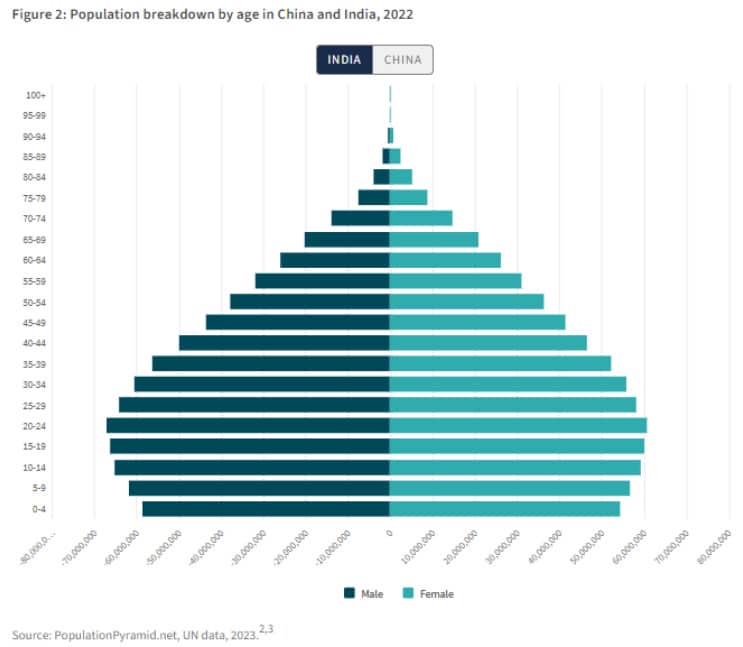

A positive demographic backdrop is among the factors that help explain the strength of the economy. India last year surpassed China to become the world’s most populous nation. It is also the only major economic power that could be described as “young”. Moreover, with 44 per cent of people under 25, India will stay that way for some time. Births will continue to exceed the labour replacement rate for the foreseeable future, unlike in China (see Figure 2).

Lured by rapid economic growth and a growing workforce, international capital has been flooding into the country in recent years. Prime Minister Narendra Modi is looking to turn India into a manufacturing hub through programmes like “Make in India”, which contains a package of incentives to attract global companies. A host of multinational firms such as Apple, Samsung, Kia and Airbus have been building up manufacturing capacity in the country as they seek a cheaper and friendlier alternative to China.

Apple, for example, plans to make roughly a quarter of all iPhones in India within two-to-three years.4 This will help the company minimize its dependence on China. Foxconn, a Taiwanese electronics manufacturer and major Apple supplier, is spending $1.5 billion to set up shop in India as well.5 Foreign direct investment (FDI) totalled $71 billion in the 2022–23 financial year, and India’s information technology minister is targeting $100 billion in annual flows “in the next few years”.6

Investing in India

Historically, it has not been straightforward for international investors to invest in India but that is changing. The country’s economic success has in recent years been accompanied by a rise in the number of exchange-traded funds, giving international equity investors access to one of the world’s best performing markets. The benchmark Sensex index last year surged 19 per cent in US dollar terms.

Demand for corporate bonds has also been buoyant in recognition of this economic success story. The extra yield investors demand relative to government debt has fallen while the size of the market has mushroomed, with debt outstanding having grown at around nine per cent a year over the past five years.7

By contrast, international investors have been largely absent from the country’s government bond market. India issues debt primarily in its own currency, in contrast to other emerging market nations which frequently issue foreign currency-denominated bonds. So the only option has been to participate in the local-currency market.

Although local-currency bonds run the risk of adverse exchange-rate movements, they can offer attractive returns. Furthermore, returns from India’s sovereign bonds tend to be relatively uncorrelated to the returns generated by other bond markets, thus helping to boost portfolio diversification.

The problem is that investing in the Indian market has until now involved jumping through a series of bureaucratic hoops. Not only do international investors have to accept the risk of the rupee depreciating, the rupee itself is not fully convertible. Transacting in Indian bonds is notably more complex than in other EM local-currency markets.

Delhi’s imposition of a withholding tax of as much as 20 per cent on the coupon payments and capital gains received by foreigners has been another barrier to international investment. While other developing countries, such as Colombia and Brazil, also have a withholding tax regime, they are the exception rather than the rule. That makes these countries’ bonds comparatively less attractive, meaning international investors will demand recompense in the form of higher yields or prefer similarly rated sovereign exposure with a lower tax burden.

Unlike many other nations’ bonds, Indian debt is not euro clearable. From international investors’ standpoint, having to clear trades in India means they do not have the security of dealing with a third party clearing house that is well known and trusted internationally. Clearing transactions in India also adds complexity as there is an extra layer of rules to abide by and the operating hours are different. That could be especially problematic for US managers, some of whom may have to employ extra staff just to be able to settle trades.

A new era for Indian bonds

As a result of these drawbacks, the Indian market has been excluded from global sovereign bond benchmarks, creating the biggest barrier of all to greater international involvement. Foreigners own just two per cent of India’s $1.2 trillion outstanding sovereign debt.8

However, this is about to change as a result of India’s inclusion in the JP Morgan EMBI indices from June 2024. Although Delhi began discussing the inclusion of its securities in global indices as far back as 2013, it wasn’t until April 2020 that the Reserve Bank of India introduced a series of securities that were exempt from any foreign investment restrictions under a “fully accessible route”. There are now 23 Indian government bond issues, with a combined nominal value of $330 billion, eligible for inclusion in the world’s most widely tracked emerging-market bond index.

This, together with the effective disappearance of what were once two of the index’s biggest markets – Russia and Turkey – over the previous few years, along with persistent concerns over economic and geopolitical risk in China, has resulted in international investors warming to Indian government debt, which should provide diversification opportunities. JP Morgan said its decision came after 73 per cent of benchmarked investors voted for the country’s inclusion.9

From June, Indian bonds will make up one per cent of the JP Morgan index. Each subsequent month they will make up an additional one per cent of the index until they eventually comprise ten per cent. With around $230 billion tracking the benchmark, that should ultimately lead to $23 billion flowing into the market.

Further inflows are likely to result from Bloomberg’s decision in March to also include Indian bonds in its local-currency government indices from January 2025. As with JP Morgan, it says Indian bonds will be included in a phased manner spread over ten months.

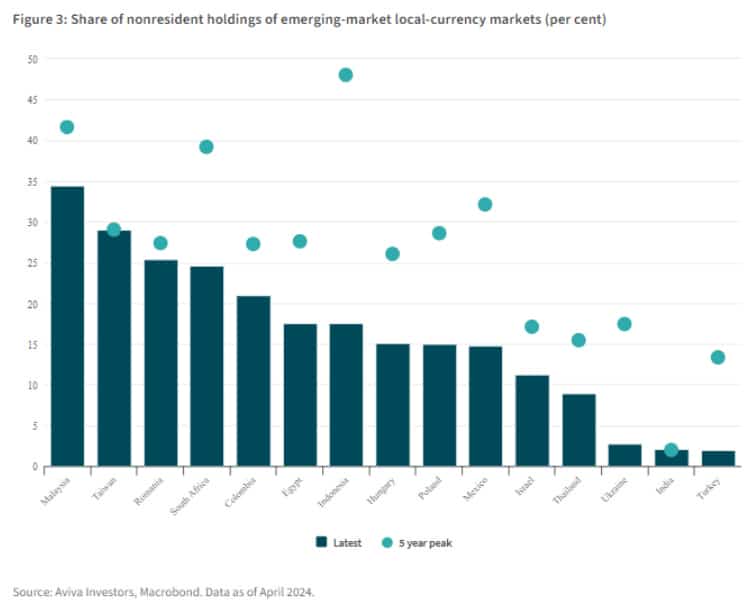

While Figure 3 shows the extent to which foreigners have scaled back exposure to almost all EM local currency debt markets, India is amongst those markets with the most scope to attract foreign investment flows.

With Indian government bonds offering a nominal yield of just above seven per cent, or roughly 2.5 per cent in real terms on a forward-looking basis, the market is attractive from an investor’s standpoint, especially given India’s economic resilience to the external backdrop.

While overall debt remains high by emerging-market standards at around 80 per cent of GDP, this is broadly in line with countries such as South Africa and Brazil. But whereas relatively weak economic growth means both these latter nations are struggling to get debt down, rapid growth should enable Delhi to make progress in reducing the debt burden.

The Indian government aims to reduce its deficit to around 4.5 per cent of GDP in the coming years. While that is large relative to the pre-pandemic period, much of this increase is explained by increased government spending on infrastructure. That should in turn help buttress economic growth for some time to come, aiding Delhi’s efforts to finance its deficit.

The world’s biggest election

Before India’s bonds are integrated into the index, its citizens are going to the polls in what will be the world’s biggest democratic exercise. Almost one billion people are registered to vote in a seven-phase process that will take six weeks between April 19 and June 1.

Modi, and his ruling Bharatiya Janata party look certain to win the vote. Although the party’s brand of Hindu nationalism has risked stoking social tensions, the prospect of continuity in economic policymaking is likely to mean international investors put such concerns to one side, at least for now.

And I came back from my trip reassured that India is in a very different position to other nations with so called “strong-men” leaders, who often single-handedly hold the policymaking reins.

The conversations I had during my time in the country bolstered my sense of the high quality of India’s financial and regulatory institutions, and the calibre of the people who lead them. That should help restrain any urge among policymakers to pursue economic growth at any cost. In any case, the government is well aware its recent focus on prudent economic management has been paying dividends.

While Indian bonds do not look especially cheap at current levels, my trip reinforced our positive outlook on the market and we have been adding exposure to India ahead of this summer’s benchmark inclusion. The prospect of sustained inflows in the coming months offers reassurance that downside risks are limited.

Moreover, while India, as a big importer of commodities, remains vulnerable to the threat of higher commodity prices, its economy has become more resilient in recent years. Stronger buffers in turn mean Indian bonds have a fairly low correlation to emerging-market peers. That could encourage many other investors to build overweight exposure as they finally get to join India’s party.

As my plane took off, I had one last glimpse of another urban sprawl – this time of New Delhi, which seemed to have expanded even over the course of my brief time in India. I was struck anew by a sense of the vast opportunities that are likely to emerge in this huge, diverse and fast-changing country over the coming years.

References

1. “Data updates and errata”, The World Bank, December 2023.

2. “Population pyramids of the World from 1950 to 2100: China”, PopulationPyramid.net, 2023.

3. “Population pyramids of the World from 1950 to 2100: India”, PopulationPyramid.net, 2023.

4. Rajesh Roy and Yang Jie, “Apple Aims to Make a Quarter of the World’s iPhones in India”, Wall Street Journal, December 8, 2023.

5. Rohan Goswami, “Apple iPhone maker Foxconn to invest $1.5 billion in India as it looks to build beyond China”, CNBC, November 28, 2023.

6. “India eyeing $100bn annual FDI over next few yrs: Min” The Times of India, January 18, 2024.

7. “India corporate bonds: Outstanding: value”, CEIC, December 2023.

8. Subhadip Sircar and Cynthia Li, “Foreign money to help PM Modi push near-record India sovereign bond sales”, Business Standard, January 25, 2024.

9. Ira Dougal, “Explainer: What India’s inclusion in JPMorgan’s bond index means for its markets”, Reuters, September 22, 2023.

")

Platform To Digitally Trade Corporate Bonds")