By Benoit Anne, Managing Director, Investment Solutions Group

While there have been plenty of fears in global markets in the recent past, we believe that the fixed income fear of missing out (FIFOMO) is going to be the new fear that fixed income investors will soon be facing, and a positive one. Given the much improved macro backdrop, including stronger central bank signals and a favorable valuation landscape, this may possibly be an attractive opportunity to increase allocation to the asset class, in our view.

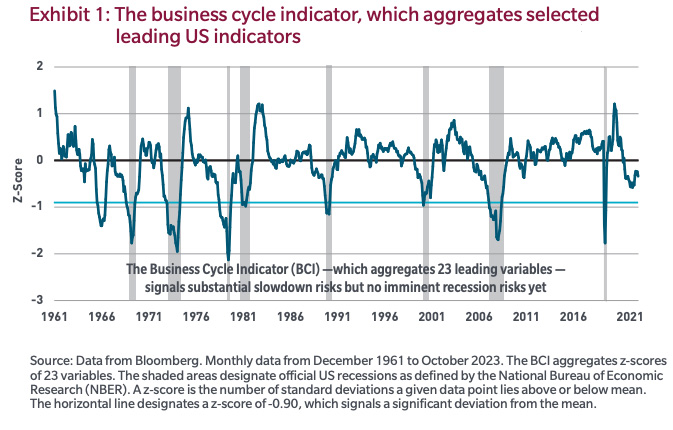

A Goldilocks macro outlook seems to be lining up. At this juncture, the risk of recession in the United States seems to have fallen, reflecting the resilience of the US consumer combined with the robust fundamentals of the corporate sector. The US economy is in slowdown mode, but the magnitude of the growth shock appears insufficient to warrant recession alarm calls. Our business cycle indicator — while signaling some slowdown risks — indicates no imminent recession. (Exhibit 1). On the inflation front, progress has been made, and it is now reasonable to think that core PCE, the inflation measure that matters most to the US Federal Reserve, will slow to around 2% next year. More important, the Fed is signaling that the tightening cycle is over. This means that we are finally ready to transition away from the dreaded fear-of-the-Fed macro regime, paving the way for a much more supportive backdrop for fixed income.

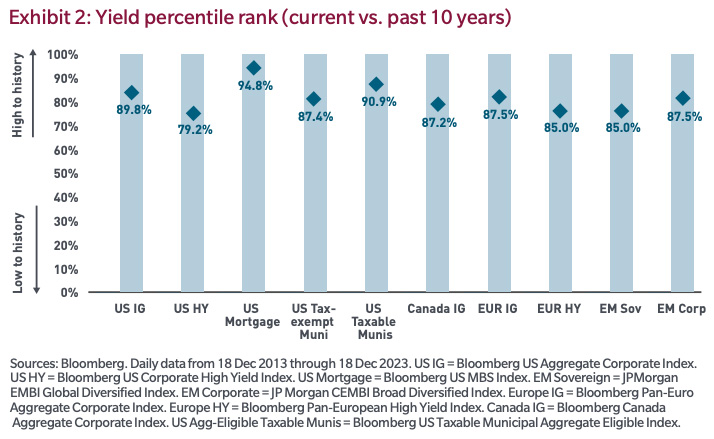

The fixed income valuation picture remains compelling. Fixed income valuations are relatively attractive for the investor with a long-term horizon, in our view. This is particularly true for total yields, which are attractive by historical standards, even after the recent rally. Looking at the percentile rank of current total yields over the past ten years, most asset classes rank in the high 80s or 90s (Exhibit 2). It is true that credit spreads in some sectors look stretched, but the total yield valuation, which includes both a rate component and a credit spread component, is important as it has been a primary driver of expected total returns. In addition, the spread valuation dispersion offers interesting opportunities for active asset managers to identify relative value strategies.

Also read: Why Park Cash In Term Deposits?

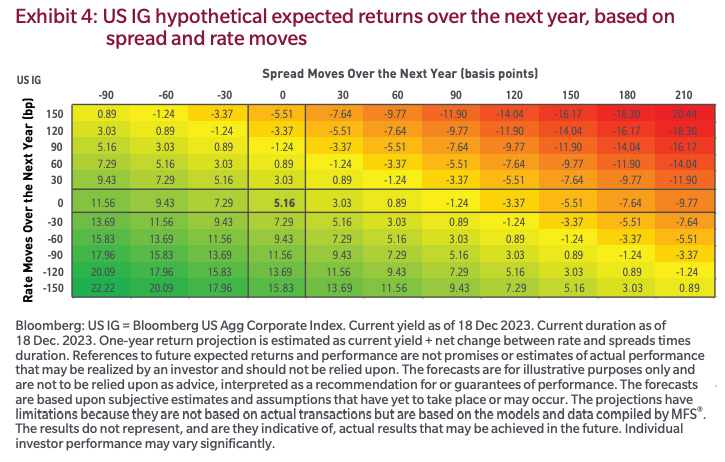

Entry points do matter in fixed income. Given the attractive level of current yields, the outlook for expected returns has improved considerably. This is because there has historically been a strong relationship between starting yields like today’s and robust subsequent returns. For instance, at a starting yield of 5.16% for US investment-grade, the median return for the subsequent five years — using a 30-basis-point range around the starting yield — stands at 5.97%, with a return range of 3.36% to 7.17% (Exhibit 3). In addition, the prospects for fixed income expected returns have been strengthened by the recent signals of future rate cuts from the major central banks. Analyzing the heat map for US investment grade, it is clear that the likelihood of higher hypothetical returns has gone up, especially with the strong possibility of rate cuts in the pipeline based on recent Fed policy signals. Specifically, based on an entry yield of 5.16% and assuming no spread move over the next year combined with a drop in rates of 60 bps, a return of 9.43% in one year could be realizable (Exhibit 4). Specifically, the one-year hypothetical expected returns are simply computed as the sum of the starting yield minus the combined move in rate and spreads multiplied by the index duration. For example, based on a starting yield of 6% and an index duration of 7, if the combined spread and rate move is a decline of 50bp (i.e. 0.50%) over the next year, then the one-year expected return will be estimated to be 9.5% (6% – (-0.50% x7)).

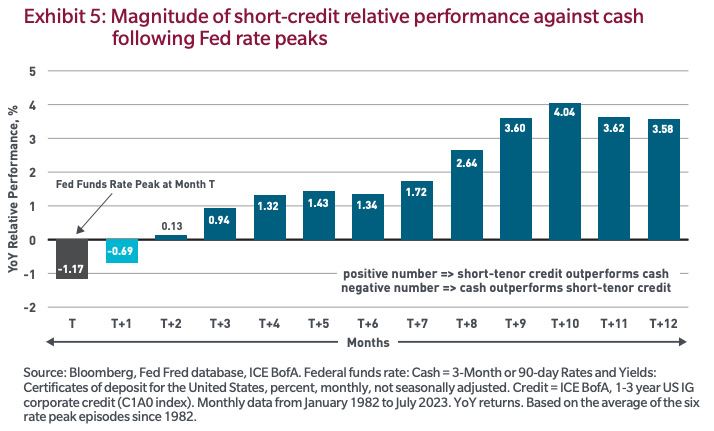

It may be time to move away from cash and back to fixed income. Cash allocations continue to be significant given the investor fear of deploying risk, especially after the past two challenging years for global markets. We stand at an important inflection point, however. Typically, shortly after the peak of the central bank policy rate has been reached, cash starts underperforming credit. This is precisely where we are right now (Exhibit 5). Going forward, the probability of cash outperforming credit is likely to drop, especially given the expected rate cuts in the pipeline.

It may be time to move away from cash and back to fixed income. Cash allocations continue to be significant given the investor fear of deploying risk, especially after the past two challenging years for global markets. We stand at an important inflection point, however. Typically, shortly after the peak of the central bank policy rate has been reached, cash starts underperforming credit. This is precisely where we are right now (Exhibit 5). Going forward, the probability of cash outperforming credit is likely to drop, especially given the expected rate cuts in the pipeline.

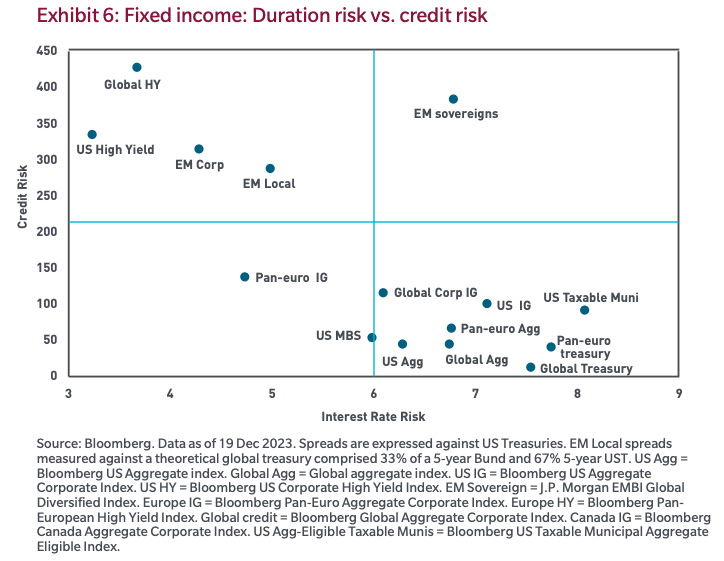

We believe the opportunity set in fixed income is extensive. There is something for everyone in fixed income, depending on the investor’s risk appetite, investment needs or other objectives. Fixed income, of course, involves both duration risk and credit risk. The combination of the two gives us a highly diversified map of sub-asset classes (Exhibit 6). We are now constructive both on duration and credit, and we therefore favor the riskier end of the fixed income spectrum, especially emerging market debt and European high yield. This is because of the more favorable macro outlook and the attractive entry levels.

")

Platform To Digitally Trade Corporate Bonds")