From Mawer Credit Team

When this piece was being written, Boeing had not filed their US$25 billion shelf prospectus and the company was a downgrade candidate to high yield (HY) at both Moody’s and S&P which would qualify them as a “Fallen Angel”. The term “Fallen Angel” is often paired with its opposite, a “Rising Star” which is a bond that has moved from a HY rating up to investment grade (IG). Downgrade risk remains for Boeing, although their new, incremental $10 billion USD credit facility and a rumoured $10-15 billion USD equity raise will help the struggling Industrial company manage their cash balances for the time being. That said, we decided it would be interesting to highlight the importance and impact that a Fallen Angel has on both the IG market, and, more importantly, the HY or “Junk” bond market.

The Fallen Angel premium (the spread between IG and HY bonds) has dwindled towards this year’s low as credit across rating categories continues to rally. Year-to-date, the market produced only 5 Fallen Angels versus 14 Rising Stars. Under the methodology used for the ICE Index, when a company is downgraded by 2 out of 3 rating agencies (Fitch, Moody’s or S&P) to HY, it moves out of the IG index and into the HY index. This often creates a wave of forced selling of these bonds as large investment grade only investors such as pension funds and asset managers cannot hold HY bonds in their portfolios. The other large pool of sellers are index type accounts that are precluded from holding bonds that are not in the IG index. They need to reallocate these funds to new additions that take the place of the Fallen Angel in the index at the end of the month. Through this rebalancing, spreads widen, and the issuer in question would see interest costs increase substantially if they were to refinance debt. At the same time, their ability to borrow money decreases measurably, as the HY market has less liquidity than the IG market and cannot accommodate the “jumbo” financings that are often completed by IG issuers.

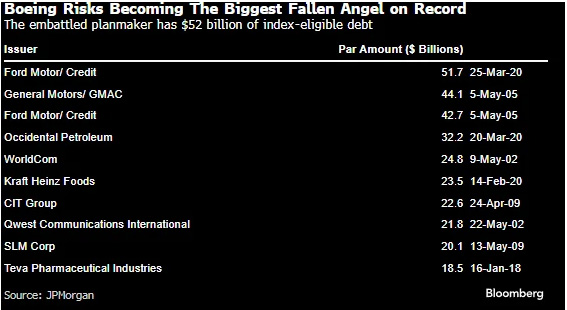

Switching back to Boeing specifically, if the company’s credit rating is cut to junk status, it would be the largest Fallen Angel ever with more than US$57 billion of bonds outstanding. The chart below shows the most recent Fallen Angels in the U.S. market. Three of the largest have already moved back to IG status (Ford, GM and Occidental).

What is interesting is that despite Boeing’s well publicized challenges and concerns expressed by the rating agencies, spreads have not widened as one would expect. As an example, Boeing’s 6.259% 2027 bonds’ spread widened ~4bps when headlines pointed out the risk that Boeing might fall out of the IG index. In contrast, when Ford was struggling pre-downgrade in March 2020 (also well telegraphed), their bonds gapped out 10 to 20bps on each trade point and liquidity dried up. The bid/ask on Boeing also hasn’t changed as we would have expected, indicating that at a high level, liquidity has not been materially impacted. In the days following the news of Boeing’s potential equity deal, spreads have snapped back in almost 10bps, putting the week over week change at -6bps. The news has also boosted the company’s shares in a bullish signal from equity investors. An equity offering would go a long way to keeping the credit rating agencies at bay for the time being, but the airplane manufacturer is not out of the woods yet and remains on our radar (no pun intended) for a potential ratings action and buying opportunity.

This article was originally published here.

")

Platform To Digitally Trade Corporate Bonds")