From QIC, Liquid Markets Group

- The J.P. Morgan Asia Credit Index (JACI) suite of indices expanded to include a new JACI Asia Pacific Index (JACI APAC) in 2023. The new index includes USD-denominated debt from the Asia Pacific region, expanding coverage of the existing JACI series by introducing new markets including Japan, Australia and New Zealand.

- The inclusion of Australia in JACI APAC provides investors with additional incentive to consider bonds from Australian corporate issuers in USD, presenting an opportunity to further diversify portfolios with exposure to high-quality, stable issuers.

- Investors can, however, replicate JACI APAC’s Australian credit allocation with a USD-hedged investment into AUD credit and, in doing so, can achieve a higher yield, higher credit quality and greater diversification.

- Actively monitoring AUD and USD debt valuations through time and actively managing security selection can add additional value.

- The AUD corporate credit market enjoys healthy liquidity, which has deepened recently as record volumes of primary market activity have been met with robust investor demand.

- We attribute some of the strong demand to new allocations from Asian investors, who are drawn to the relatively attractive yields and spreads on offer for investment grade credit in a developed market.

With an overlapping time zone, strong governance standards, an actively traded G10 currency and relatively attractive yields, Australian fixed income has long held the interest of Asian investors.

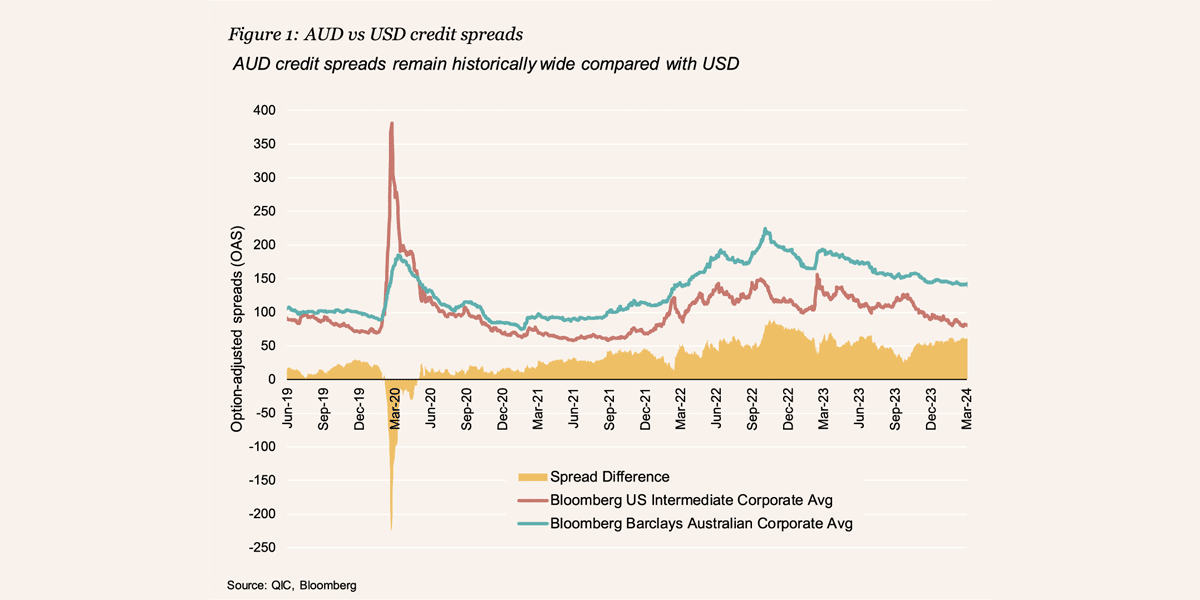

The Australian investment grade (IG) credit market currently presents a particularly compelling opportunity for offshore investors, as AUD credit spreads remain relatively wide despite the significant tightening of credit spreads in other major developed markets (refer Figure 1). With this attractive relative value in AUD credit we are seeing a notable increase in Asian investor interest in the local market over the last six months.

Also read: The Economy, The Fed, and Market Dynamics in 2024

Relative value for AUD credit

Credit spreads globally began 2024 on a positive note, continuing the rally that started after the Federal Reserve pivot in the second half of 2023. IG cash spreads in the United States and Europe have moved significantly tighter, with higher outright yields attracting strong inflows and outweighing any hesitation from investors concerning tight spreads.

While AUD credit spreads have also tightened meaningfully since the wide levels of 2022 and early 2023, the rally has lagged the recent strength in USD credit (as shown in Figure 1) which makes a rotation into AUD-denominated credit increasingly compelling with spreads almost double US spreads.

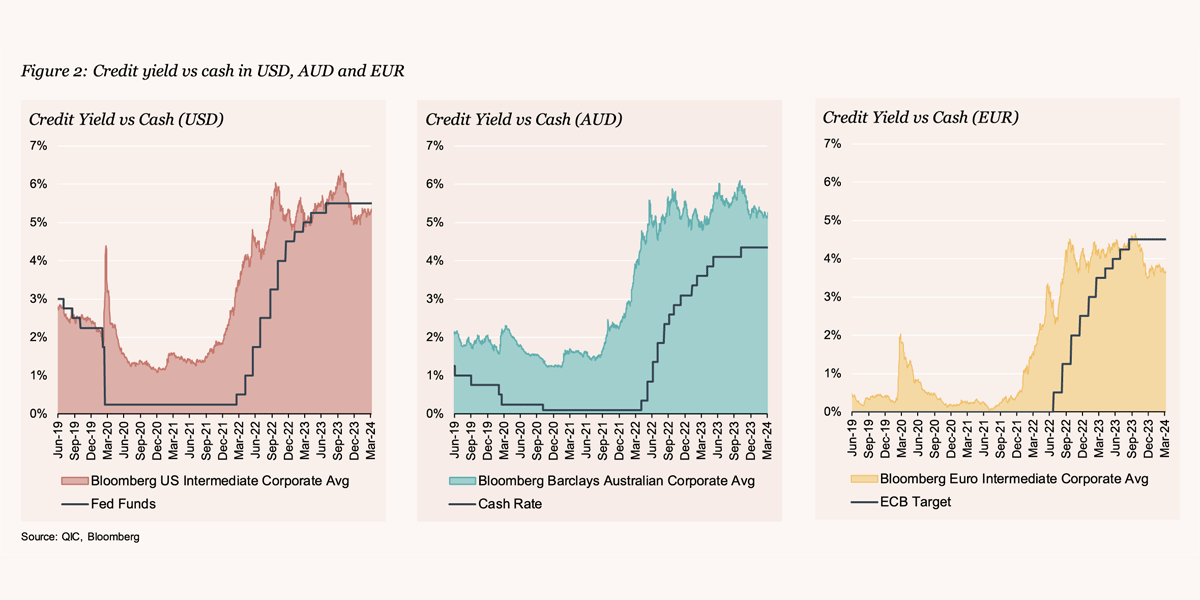

In a further demonstration of the relative attractiveness compared with USD and EUR credit, AUD is now the only market where credit benchmark yields are meaningfully above cash rates (see charts below). While inverted yield curves based on rate cut expectations will be a factor, this differential makes the Australian market an appealing destination for long-term yield-focused investors and, in our view, is likely to support spread performance moving forward.

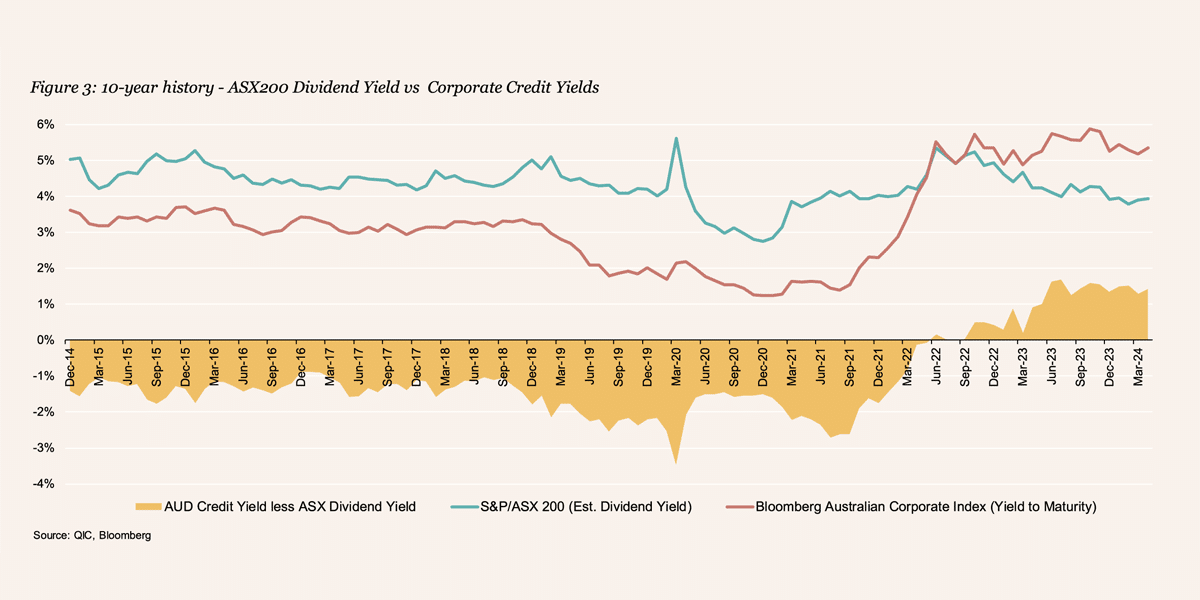

The relative value of AUD credit compared with other assets classes is also worth highlighting. With IG credit yields at 10-year highs, they are – somewhat unusually – currently offering a more attractive income than dividends expected from ASX 200 stocks (shown in the chart below).

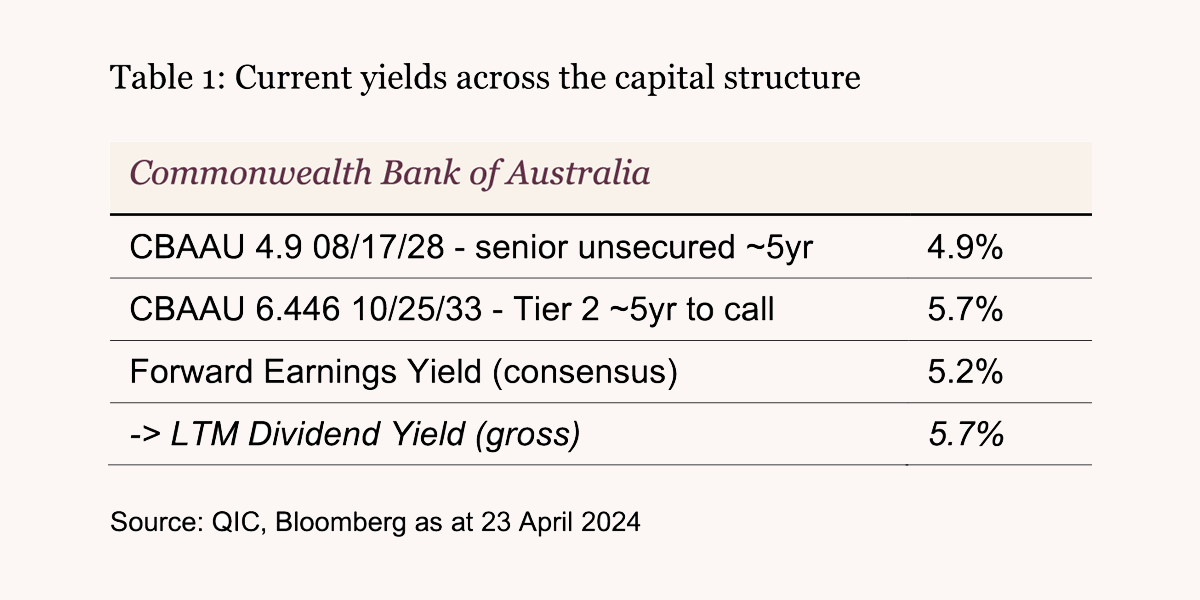

The example in Table 1, using the Commonwealth Bank of Australia at the issuer level, demonstrates how investors can earn a similar yield to equity with lower risk by moving up the capital structure into debt issuance, given the high yields currently on offer.

Liquidity of AUD credit

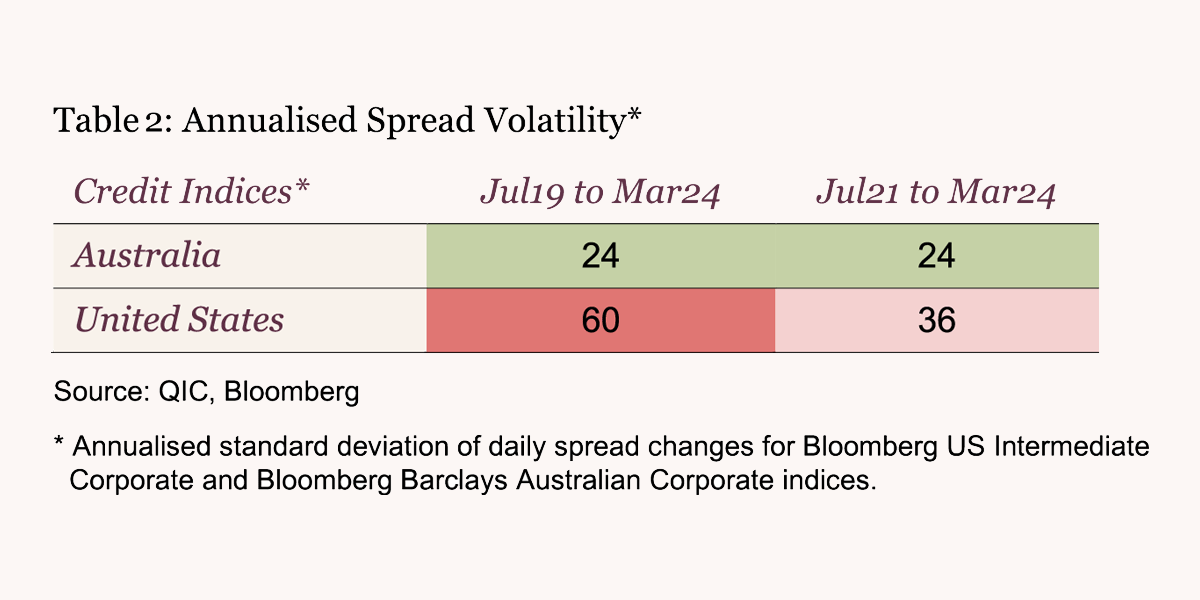

The performance of AUD credit spreads typically lags that of the larger offshore developed market peers, namely the US and European markets, in both widening and tightening cycles. While this difference is suggestive of lower volatility (see Table 2), which may be attributable to a higher average credit quality, to some extent it may also be perceived as reflecting lower liquidity compared with the deeper US and European markets.

However, we have observed liquidity in AUD credit pick up markedly post-COVID as the overall size of the market has grown and has attracted more participants – particularly from offshore. This interest in turn has encouraged more issuance, in a virtuous cycle. Anecdotally, brokers are also reporting increased secondary trading volumes, which is consistent with the increased primary market activity.

Growth in market size

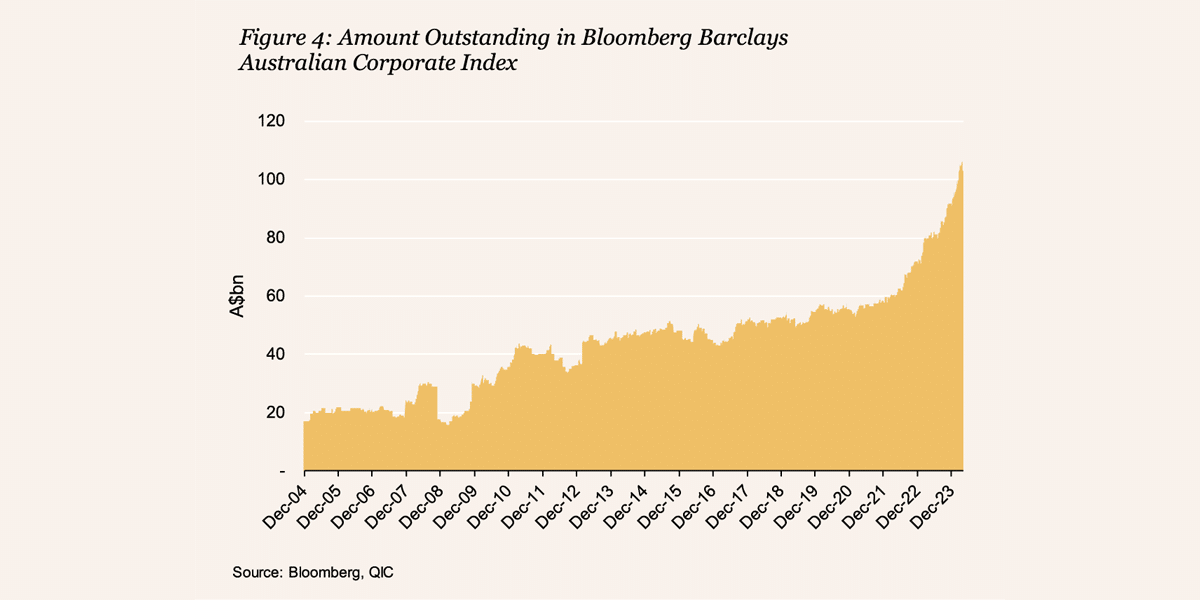

- The growth of the overall AUD credit market can be illustrated by observing the growth of amount outstanding in the Bloomberg Barclays Australian Corporate Index, as seen in Figure 4. This growth is a reliable proxy for the wider IG AUD credit market, which we estimate has grown to over A$360bn1.

Growth in investor participation

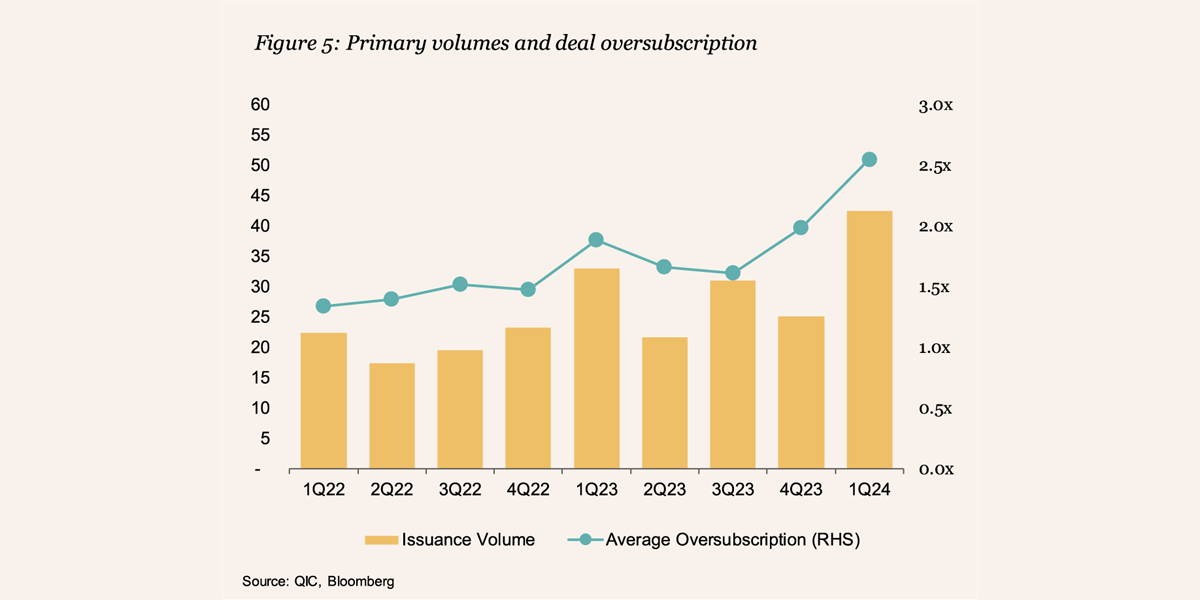

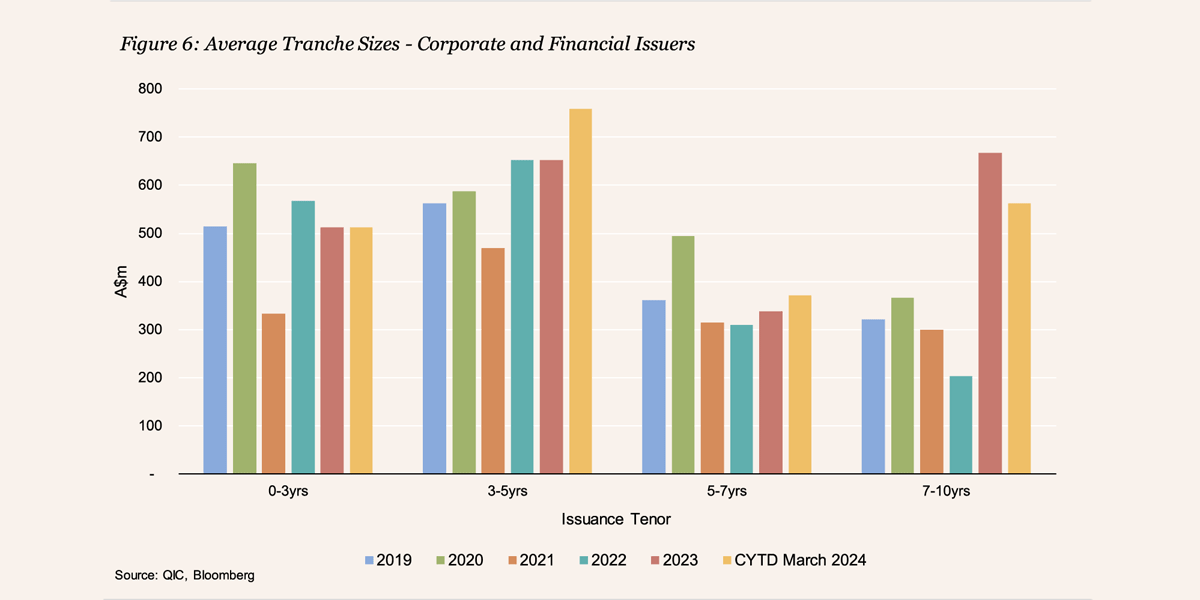

- Wider participation in AUD credit markets is evident by the notable increase in primary market orderbooks, with deal oversubscription rising significantly (a result that is even more remarkable considering the large increase in overall issuance volumes). Average tranche sizes have also increased, commensurate with the market’s growth, offering deeper liquidity on each line. Refer to Figures 5 and 6 below.

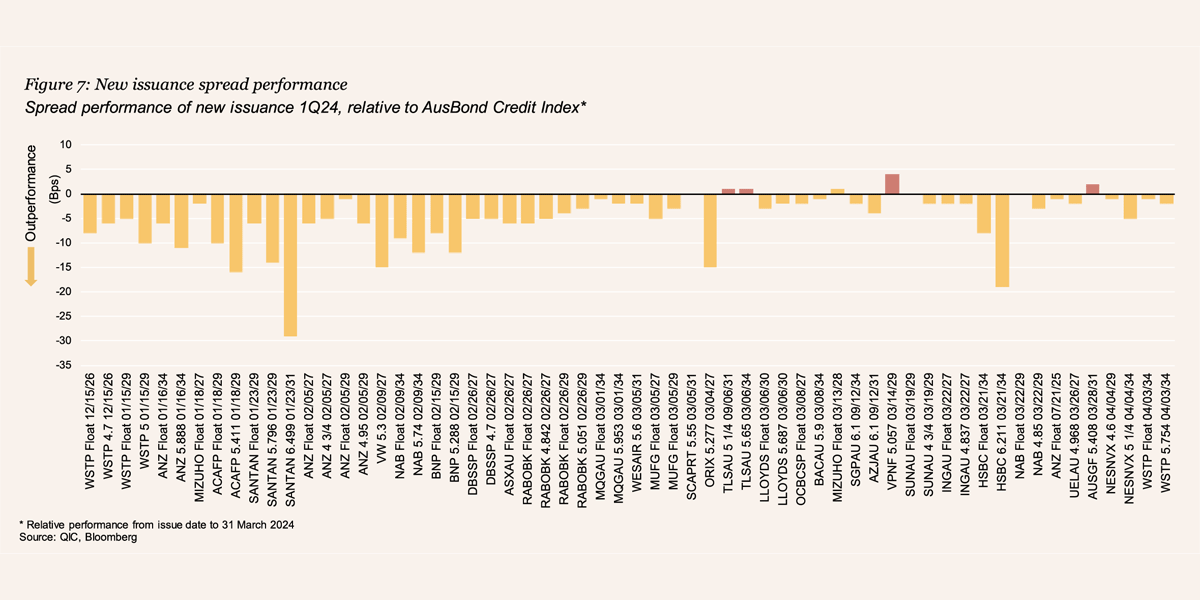

- The strong demand and oversubscription in AUD primary markets has seen new issues pricing with increasingly smaller concessions, a dynamic which can be observed in subsequent secondary market performance in our view (refer Figure 7). Active management provides the flexibility for selective participation in the most attractive primary market deals.

AUD credit opportunities relative to Australian issuance in JACI APAC

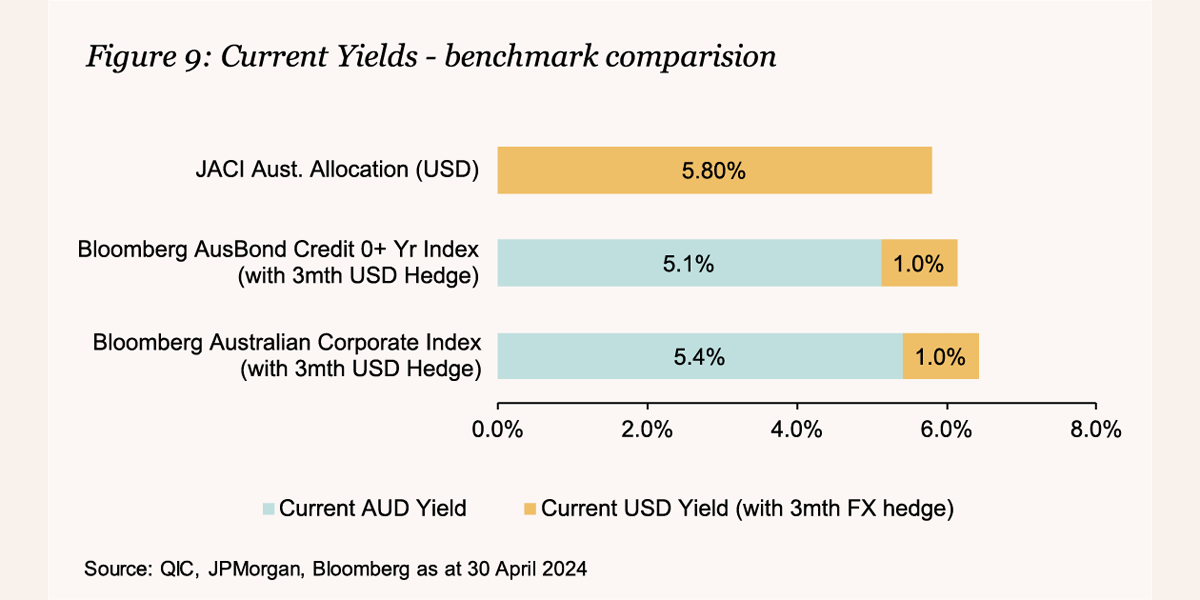

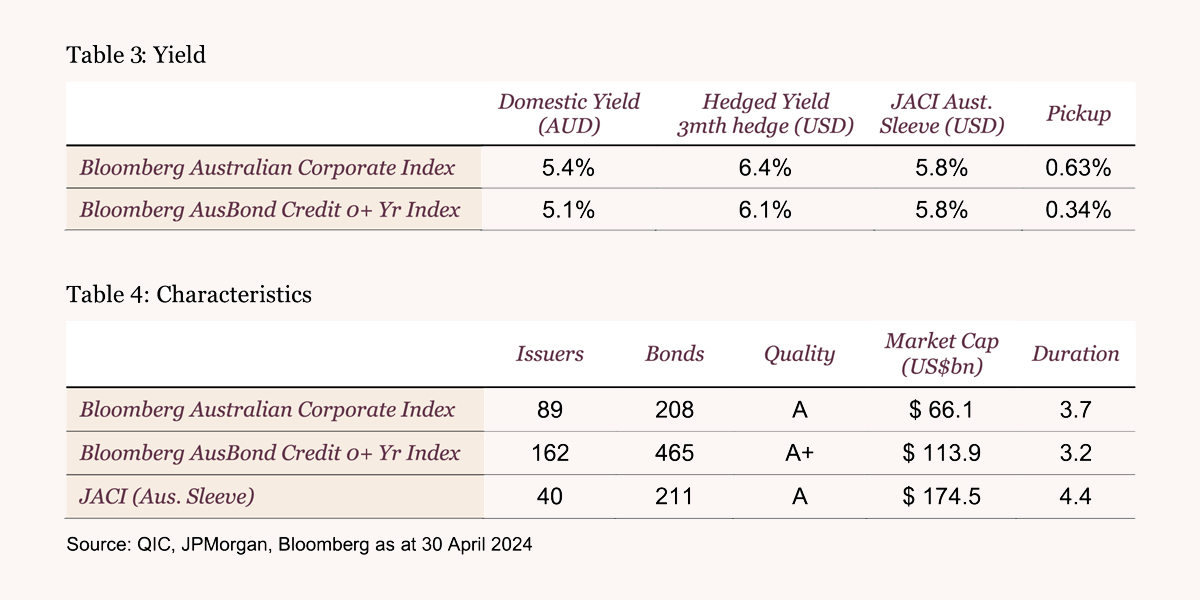

The JACI APAC Index included USD-denominated bonds of 40 Australian issuers at 2 April 2024 (the “Australian allocation”). Investing in AUD credit and hedging to USD as an alternative to JACI’s USD-denominated Australian allocation can provide higher yields while also offering lower risk (i.e. higher average credit quality, lower duration, greater diversification).

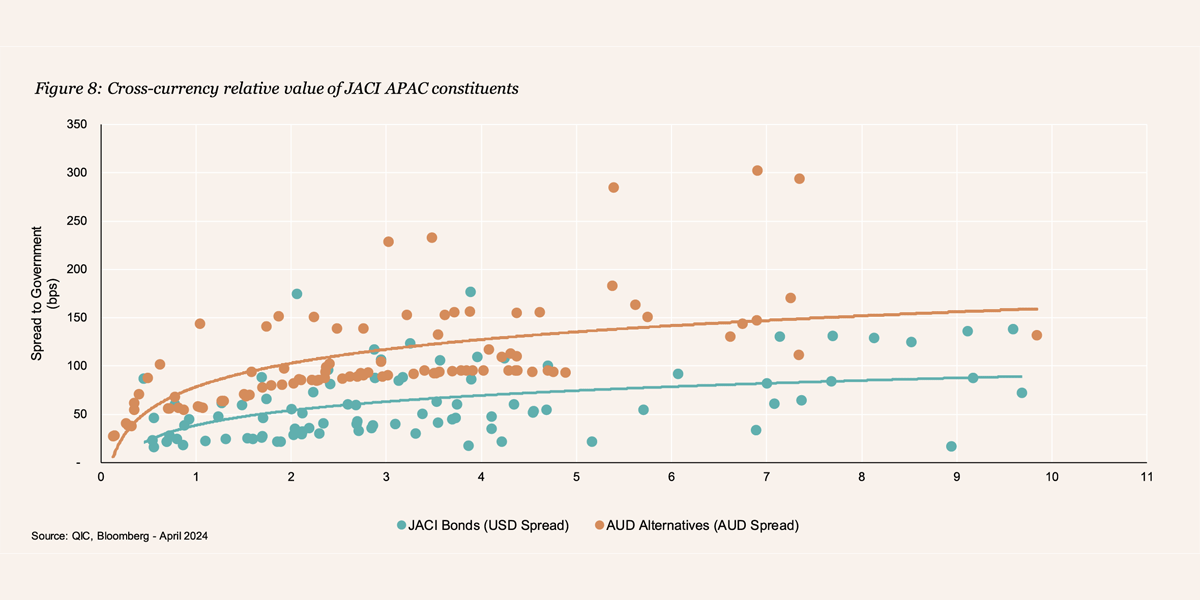

The credit exposure in JACI APAC’s Australian allocation can be replicated by investing in the 17 index constituents that also issue in AUD, or by substitution with a broader and more diversified portfolio of AUD credit:

- Direct investment in the 17 JACI APAC constituents that also issue in AUD offers higher spreads in the local currency than in USD, a reversal of the home market bias often observed in global credit markets. The chart below shows spreads over government bonds for the USD-denominated issuance of Australian constituents in the JACI APAC relative to AUD issuance from those same issuers.

- Substitution of the Australian allocation of the JACI APAC Index with a more diversified portfolio of AUD credit offers the ability to simultaneously achieve a higher yield (with lower duration), greater diversification and a higher average credit rating.

Other advantages

Time zone synergy

The common time zone with Asian markets facilitates real-time communication and transactions, providing a strategic advantage for investors in Asia. This synergy enhances the efficiency of investment decisions and market access, making it easier for Asian investors to engage with the Australian market.

Engaging an Australian fund manager can provide Asian investors convenient access to local market experts, including strategists, traders, portfolio managers and Australian-based credit analysts.

Governance and currency stability

Australia’s governance standards are robust. This is demonstrated through stable sovereign credit ratings of AAA/Aaa/AAA from Standard and Poor’s, Moody’s and Fitch together with strong governance rankings in the 93rd percentile (above the United States at 72.9%) from the World Bank’s latest data set of Worldwide Governance Indicators2.

The Australian dollar is an actively traded G10 currency that benefits from Australia’s strong economic fundamentals, prudent fiscal policies and robust legal framework. This stability is a key factor for investors seeking to minimise currency risk in their international investments.

Conclusion

The Australian credit market stands out as an attractive investment destination for Asian investors, offering a combination of historically attractive credit spreads and yields, governance strength, time zone alignment and hedging efficiency.

Originally posted on QIC

Citations

- AUD Investment Grade Corporate issuance currently outstanding with tranche size >A$100m.

- Home | Worldwide Governance Indicators (worldbank.org) Daniel Kaufmann and Aart Kraay (2023). Worldwide Governance Indicators, 2023 Update (www.govindicators.org), Accessed on 03 April 2024

Platform To Digitally Trade Corporate Bonds")