At the start of the year, U.S. exceptionalism, which has prevailed for over a decade, was widely expected to persist. Since then, however, several factors have coincided to test the U.S. exceptionalism theme.

1. The U.S. technology sector—the primary driver of U.S. equity market performance in recent years— has been significantly challenged as investors question stretched valuations and earnings expectations.

2. Growth expectations for the U.S. economy have been revised downward in response to rising policy uncertainty, and policy proposals that have proven to be more severe than widely expected.

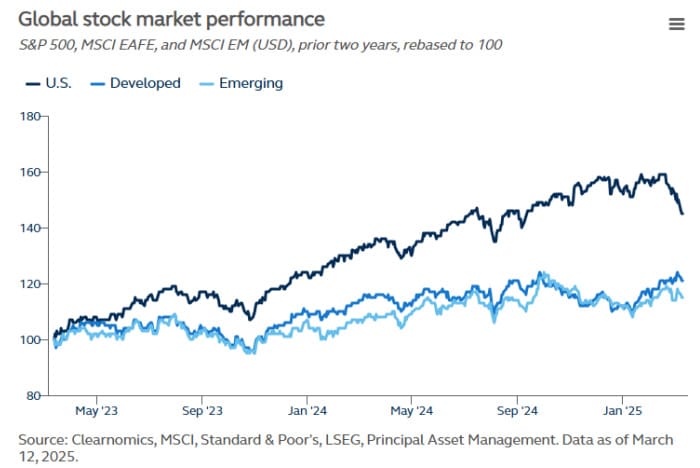

3. German lawmakers have passed a landmark spending package that promises to unlock almost a trillion euros for defense and infrastructure, ending decades of budget austerity and triggering hopes for a broader European fiscal shift. With Germany’s notable fiscal expansion and European equities outpacing the U.S. by nearly 20% YTD, investors are starting to question the long-standing theme of U.S. exceptionalism. While structural challenges remain, a shift in sentiment—and leadership—may be underway.

Germany’s massive fiscal shift

President Trump’s decision to suspend military aid to Ukraine in early March, plus his evolving approach to global security, has prompted a significant re-think on defense spending in Europe and accelerated a long-awaited fiscal shift in Germany.

In response, the German government has changed its constitutional rules, bringing the following changes:

a. The creation of a €500bn infrastructure investment fund.

b. Exemption of defense spending above 1% of GDP from the debt brake rule, which restricts annual structural deficits to 0.35% of GDP (This effectively permits open-ended borrowing for defense).

c. Easing of fiscal constraints for federal states.

Taken at face value, Germany is set to embark on a major fiscal expansion—over €1 trillion—far exceeding expectations. While a policy shift wasn’t a surprise, the scale marks the biggest change in Germany’s fiscal approach since reunification 35 years ago. The reforms could raise allowable structural net borrowing by more than 2% of GDP annually, though questions remain about how quickly the funds can be deployed.

Also read: Credit Under The Microscope

The expected impact on Germany’s growth outlook

Germany’s planned fiscal expansion remains uncertain in timing and composition, but its scale suggests lasting economic impact. While the effects will take time to materialize, and U.S. tariff threats pose headwinds, near-term growth in Germany is likely to remain weak—though slightly improved from recent trends. We do expect the German economy, after two consecutive years of contraction, to grow by 0.2% this year. However, once the fiscal impulse kicks in, the impact to economic growth will be significant, providing an estimated 0.5% boost to German GDP growth over the next few years. We expect Germany’s economy to grow by 1.5% in 2026 and 2.0% in 2027. If the infrastructure investment is paired with structural reforms like deregulation, Germany’s fiscal shift could lift productivity and support long-term growth near 2%—similar to that of the U.S.

A boost for Germany is a boost for Europe

Germany, which makes up about a third of Euro area GDP, is poised to lift broader European growth through its fiscal expansion. At the same time, the EU has proposed a modest but supportive fiscal shift, including looser budget rules to enable more defense spending, a “national escape clause” for member states, and a new €150 billion loan facility (SAFE) to support investment. While the EU-wide impact will be smaller than Germany’s, it should still provide a 0.1–0.2% boost to Euro area GDP in the coming years. We forecast Euro area growth at 0.7% in 2025, overwhelmed by the near-term impact of tariffs, rising to 1.2% in 2026 and 1.4% in 2027.

From the inflation perspective, the fiscal stimulus provides only a marginal impact as the additional spending is not directly influencing consumer income or spending. Yet, as the ECB has already been growing more cautious around further rate cuts in recent weeks, the slightly stronger medium-term outlook for Europe likely means that the ECB will perceive it less necessary to cut policy rates meaningfully below neutral. We expect only two more 25bps policy rate reductions in 2025, taking the deposit rate down to a floor of 2%.

Improving, but not yet exceptional

Clearly, Germany’s fiscal shift is good news for Germany and the Euro area economy, and this has been reflected in market dynamics of late. Yet, while the last few weeks may represent a game-changing moment in Europe’s economic history, investors should be skeptical that it has sufficiently raised Europe’s outlook such that it can genuinely challenge the U.S. exceptionalism theme.

Not only does Europe face looming near-term risks, but the fiscal shift has not changed the narrative around some of Europe’s important structural obstacles, including strict regulatory constraints and labor market inflexibility. So, while the U.S. economy is undoubtably facing serious headwinds in the near-term, the potential for a further easing in regulatory policies and a drive to improve labor market efficiencies are still top of mind for investors, enabling the U.S. exceptionalism narrative to be maintained in the period ahead.

")

Platform To Digitally Trade Corporate Bonds")

")