Jay Sivapalan, Head of Australian Fixed Interest at Janus Henderson, discusses the path ahead for the Australian economy and what it means for the fixed interest outlook.

What are the key themes you’re watching?

With Australia having spent the best part of two years in various states of lockdown, along with international and state border closures, bridging across the resulting economic chasm has required extraordinary monetary and fiscal stimulus measures.

The key themes in 2022 relate to the normalisation of these policy measures and the re-opening of the Australian economy. Looking to the resumption of our normal economic rhythms, the economy is coming to the point where it can finally be taken off life support.

As policy measures normalise, we expect opportunities to emerge where it relates to yield curve steepness and comfort around the yield curve. As opposed to sitting in cash at 0.10% when markets have baked in a severe cash rate tightening cycle, opportunities for active asset allocation and duration management will emerge.

Markets rarely get the yield adjustments right as they grapple with the timing, speed and quantity of monetary policy tightening. This was evident during the year in February and October, which saw two of the biggest monthly bond market sell-offs since 1983. We are almost certain that volatility will remain elevated in bond markets while economies are normalising policy over the next few years – the path to normalisation is never straightforward.

Many sectors have been artificially supported through the various forms of policy support, including the term funding facility, committed liquidity facility, quantitative easing and yield curve control. As these measures are unwound, we expect semi-government bonds, residential mortgage-backed securities and major bank senior debt valuations to be affected.

Conversely, domestic re-opening winners, such as toll roads, shopping centres, consumer and housing segments represent better relative value in this environment. Meanwhile, the re-opening of international borders will support universities, airports and housing-related senior debt.

What are some key takeaways for investors from 2021?

A key lesson for investors is that central banks can quickly change course in signalling the tapering or abandonment of pandemic stimulus measures, and the market’s response can be both swift and overblown.

Markets have really struggled with a secular shift in inflation, wages, term risk premia and ultimately nominal government bond yields. Once the market prices in sufficient monetary policy tightening, especially within the context of the highly indebted housing mortgage debt in Australia, opportunities exist to take advantage of overshoots by adding back in duration.

In our experience, markets often overshoot fundamentals and we believe investors are best served by constructing portfolios based on sound principles rather than current market sentiment.

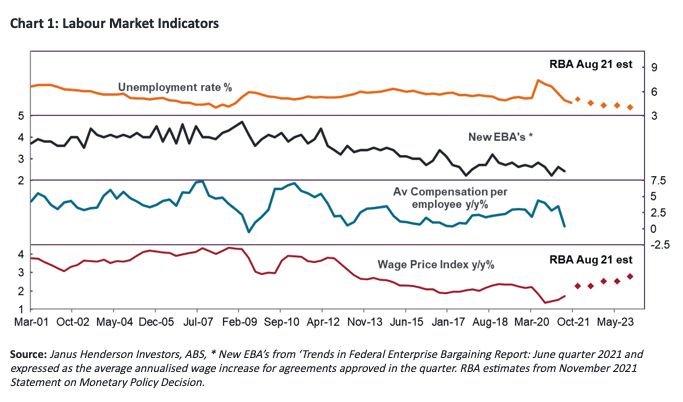

What chart is a key indicator for 2022?

The single most important chart to watch in 2022 will be wages inflation, how widespread it is and how it compares to other markets. This will be one of the last items for the Reserve Bank of Australia to meet its ‘trifecta’ preconditions (Unemployment rate close to 4%, actual inflation sustainably above 2.5%, and wages growth ≥3%) to confidently normalise.

In contrast, the US has a similar pricing path ahead for cash rates, yet has approximately double Australia’s wages inflation. How the US Federal Reserve responds has global ramifications, and we will continue to watch this closely and manage our portfolios accordingly.

As a Melbourne-based team, we have endured many months of lockdowns over the past two years and all eagerly look forward to the return to ‘normal’ life in 2022. While the emergence of the Omicron strain of COVID-19 could affect the path ahead, it is too soon to know its full impact. We are hopeful that high vaccination rates mean Australians can safely avoid more lockdowns in the year ahead.

")

Platform To Digitally Trade Corporate Bonds")